Join our daily newsletter At The Bell to receive exclusive market insights

- It’s been a rollercoaster journey for lithium investors over the past decade, with major rises and falls in the price of the precious commodity

- As the popularity of electric vehicles (EVs) rose, lithium carbonate prices soared, reaching a high of US$25,000 per tonne in November 2017

- However, this brought about an oversupply of lithium as producers went all-in on production, causing lithium prices to tumble and bottom out at US$6000 per tonne in 2020

- With the help of Elon Musk’s Battery Day event in September 2020 and a renewed outlook on the EV market, however, lithium has started to rise once more

- This means several ASX-listed miners are in strong positions to profit off a new lithium boom

- Among these are Galaxy Resources (GXY), Mineral Resources (MIN), Galan Lithium (GLN), and Prospect Resources (PSC)

- Each of these miners has the potential to ride the lithium wave higher, but it’s up to investors to decide where to place their bets

It’s been a rollercoaster journey for lithium investors who have been following the story of the precious commodity over the last decade.

Typically, demand for lithium rises as tech evolves and more devices make use of lithium-ion batteries. The high energy-to-weight ratios and slow loss of charge of lithium-ion batteries have made them the first choice for the likes of smartphones, laptops, various clean energy tech, and more.

Yet, for all these important applications, it’s the prospect of electric vehicles (EVs) that seems to have the strongest effect on lithium prices.

With a renewed focus on EVs, lithium is looking to be the big winner of 2021.

So, which ASX-listed stocks are primed to make the most of this rise?

Lithium on the ASX

A handful of listed companies — big- and small-cap alike — have a hand in the lithium production market, though some may be better-placed to profit off of the commodity than others.

Galaxy Resources (ASX:GXY)

It would be remiss to discuss lithium on the ASX without speaking of Galaxy Resources, which was once the poster-boy for Aussie lithium production.

The company has three core lithium projects: Sal de Vida in Argentina, Mt Cattlin in Western Australia, and James Bay in Quebec, Canada.

While the company considers Sal de Vida to be its flagship project, given its recognition as a Tier-1 lithium brine asset, Galaxy is so far only producing lithium from Mount Cattlin. In fact, Galaxy produced 191,570 dry metric tonnes of lithium concentrate from the project in 2019 alone.

Of course, given the weakening price of lithium over this period, Galaxy posted a $429.9 million net loss over 2019. The company was forced to scale back production at Mt Cattlin due to low demand and weak prices, and shares in the company fell from over $4 each in 2018 to less than $1 each in 2020.

However, investor interest was renewed in Galaxy when the price of lithium began to rise, and the prospect of soaring demand meant production could ramp up once again. Shares in GXY shot to over $3 each in January 2021.

Galaxy has already proven its lithium production capabilities from Mt Cattlin and is continuing to develop its over core assets, meaning the company could be well-placed to ride the 2021 lithium wave. Galaxy has a market cap of around $1.5 billion.

Mineral Resources (ASX:MIN)

While ASX-200 listed Mineral Resources is, at its core, a mining services business, the company also has some important lithium assets in Western Australia.

In fact, MIN claims its two hard rock lithium mines in WA make it one of the world’s largest owners of hard rock lithium units.

The company’s Mt Marion mine in WA’s Goldfields region was initially designed to produce 206,000 tonnes of spodumene concentrate per year but is busy being upgraded to produce 450,000 tonnes of all-in six-per-cent spodumene concentrate each year.

Mt Marian produced 133,000 dry metric tonnes of spodumene concentrate in the first quarter of the 2021 financial year.

Meanwhile, the Wodgina asset in WA’s Pilbara region is being built up to produce 750,000 tonnes of spodumene per year for over 30 years.

MIN’s exposure to other commodities and services means its share price will be less affected by lithium alone, but the company is still setting itself to be a major producer of the metal over the next few years.

Galan Lithium (ASX:GLN)

On the smaller side of the market, where there is a much easier barrier for entry for mum and dad investors, Galan Lithium holds two core projects in Argentina’s Hombre Muerto region — the same region as GXY’s Sal de Vida project.

According to the company, this region is known to host the highest-grade and lowest-impurity lithium assets across the globe.

And, with its Hombre Muerto West (HMW) project resource recently bolstered to two million tonnes of lithium carbonate equivalent, Galan owns the third-largest lithium resource in this prolific basin.

Much of the company’s success comes from prudent and passionate management, with Managing Director JP Vargas de la Vega quitting his former job as a mining executive after seeing the HMW project first-hand on a trip to Argentina in 2017.

The company’s shares peaked at 62 cents each in February 2019 but fell back below 20 cents by October 2020 as the price of lithium spiralled.

Yet, investors have started to flock back to the small-cap miner as lithium rises once again, with shares in GLN more-than-tripling in two months to hit 53 cents each in late-January.

With a market cap of $107.48 million, Galan Lithium has a whole lot of room to grow.

Prospect Resources (ASX:PSC)

Another player in the small-cap lithium world, Prospect Resource is focussing its efforts on battery minerals mining in Zimbabwe, Southern Africa.

This is important for two reasons: firstly, Zimbabwe’s government is aiming to use mining as a core source of revenue and wealth for the country, meaning mining permits are easier to obtain, and waiting periods in Zimbabwe are shorter than in many other jurisdictions.

Secondly, while companies across the world scramble to get a piece of a “Lithium Triangle” in Argentina, competition in this area is fierce. Prospect faces less competition as it builds up its flagship Arcadia project in the outskirts of Harare in Zimbabwe.

The Arcadia project is expected to be relatively cheap to build; according to Prospect’s Definitive Feasibility Study on the project, released in December 2019, the company is expecting to spend US$162 million (around A$213 million) to take the project to production.

This is particularly impressive given the life-of-mine revenue for Arcadia is over US$3.4 billion (around A$4.5 billion) over 15 years.

Prospect shares have traded for around 18 cents each in a $60 million market cap over 2021 so far.

With a strong board made up of Australian miners experienced in taking projects from exploration to production, Prospect Resources could prove to be a sturdy bet for the savvy lithium investor.

Of course, this all begs the question: why lithium, and why now?

More than they could chew

As the popularity of EVs surged over the past decade, demand for lithium carbonate surged with it.

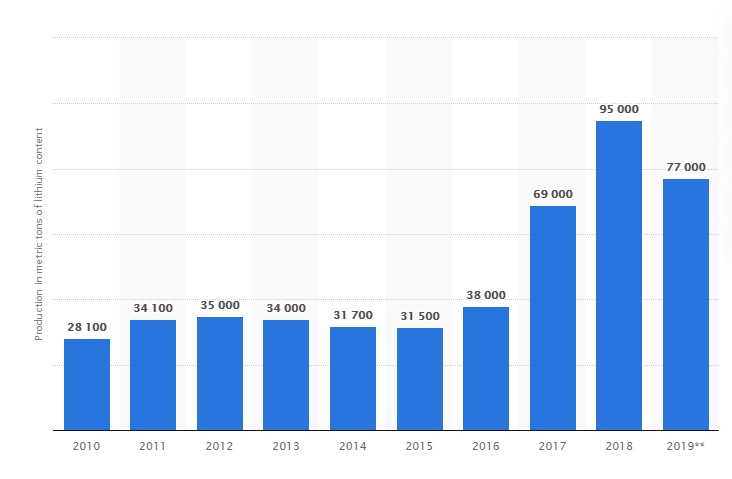

According to Statista, global lithium production was relatively stable from 2010 through to 2016, with between 28,000 and 38,000 metric tonnes of lithium content produced around the world during this time.

The battery metal then garnered the attention of producers and investors alike in 2017 when global production soared to 69,000 tonnes of lithium content. In was in November 2017 that lithium carbonate hit its all-time-high price of over US$25,000 per tonne.

Source: Statista 2021

However, while the lithium frenzy saw miners dramatically ramp up production, they were faced with an unexpected issue in 2018: the anticipated global fleet of EVs was still ramping up, and there was too much lithium to go around.

Lithium production hit 95,000 tonnes in 2018, but prices tumbled. By the end of 2018, lithium carbonate prices had more-than-halved to around US$12,000 per tonne.

This trend would continue through to mid-2020 when lithium carbonate bottomed-out at US$6000 per tonne.

Back to the future

It was the Tesla Battery Day event in late-September 2020 that saw the sentiment around lithium begin to shift.

Not only did Elon Musk’s tech empire flag its grand plans for the electric vehicle industry, but the Tesla chief also revealed the company had secured a lithium deposit in Nevada with plans to begin producing the resource in-house.

When considering Grand View Research predicts the global electric vehicle market to reach a whopping $1.2 trillion by 2027, late-2020 saw a re-reversal in the price of lithium and the commodity began to rise once more.

While still well below its 2017 glory, lithium carbonate has climbed steadily since November 2020 to now sit just above US$10,000 (around A$13,000) per tonne.

Concerns around lithium have flipped completely, with Morningstar senior equity analyst Seth Goldstein predicting the coming decade will see an undersupply of lithium, not an oversupply.

“We appreciate Tesla’s goal to secure its raw materials supply. However, we disagree with the claim that Tesla will be able to supply all its own lithium,” Seth said.

“While we view lithium as an abundant resource, with lithium present in ocean water, nearly all of the world’s lithium is not economically viable to extract at current prices.”

A potential lack of supply is already starting to see the price of lithium climb.

This means the listed miners who moved quickly to grab a hold of the lithium market over the past several years are now primed to reap the rewards.

As the price of lithium rises, the value of lithium miners will rise with it. It’s up to investors, then, to choose the play they believe will yield the greatest returns.

-1200x645-380x200.jpg)