In this feature:

- A credit explosion down under is setting the country up for a heavy correction in the years to come

- To combat economic shock, the Federal Government wants to bring in Chapter 11-style bankruptcy laws and roll back responsible lending legislation

- It comes as the country’s debt continues to grow, overshadowed by rising global arrears

- Meanwhile, mounting deferrals and a jump in lending are setting the country up for another credit crisis

- It’s something we experienced when we saw thousands of loans go sour

- While they dodged the bullet then, banks and fintechs will come under fire when the bubble bursts this time around

- But there are companies within the debt collection and technology space which are poised to grow amid the crunch

A credit explosion down under is setting the country up for a heavy correction in the years to come.

On our home turf, new policy reform is being ushered through to stimulate the economy and get Australians spending again.

While only time will tell if this has the intended effect, one thing is clear: the move will see mum and dad investors saddled with extra debt amid one of the worst recessions on record.

And while much of the focus is on the now, those looking ahead will see there’s clear winners and losers when the great Australian credit crisis hits.

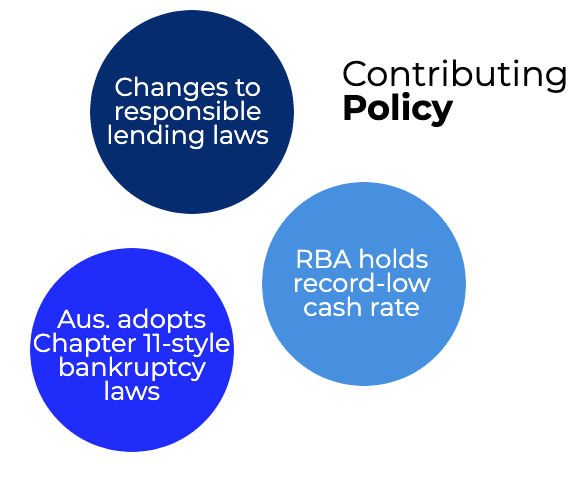

Policy reform

The credit explosion will be fuelled by a wave of policy changes, tabled by the Federal Government in recent weeks.

First, changes to Australia’s bankruptcy laws to mirror the U.S.’s Chapter 11 filings will throw a life raft to small businesses. Under the alterations, business owners have 20 days to come up with a plan to restructure debt and trade out of insolvency.

Then, news that responsible lending laws were being stripped back was welcomed by the banks. The switch is a win for them — it places extra onus on the customer to make sure they can pay back their debts.

“We can’t have a world in which, if a borrower can’t repay the loan, it’s always the bank’s fault,” RBA Chief Philip Lowe said in August.

“On a portfolio basis, we want the banks to make some loans that actually go bad because if a bank never makes a loan that goes bad, it means it’s not extending enough credit.”

RBA Chief Philip Lowe, August 2017

Coupled with the RBA’s record-low cash rate, which, in turn, fuelled modest interest rates, there’s a growing pool of cheap money readily available for consumers.

It’s a theme amplified by the booming buy now, pay later space, which encouraged a new generation of consumers to enter interest-free debt and pay it off in bite-sized instalments.

However, beyond the credit craze is a crash that poses widespread and resounding economic effects.

Debt abounds

The incoming wave of readily accessible financing is overshadowed by the impending avalanche of debt. And that idea might be easier to grapple with if we weren’t already experiencing a deficit.

Australia’s Federal Government debt totalled over $570 billion before the pandemic hit, but now that figure is forecast to blow out past $1 trillion.

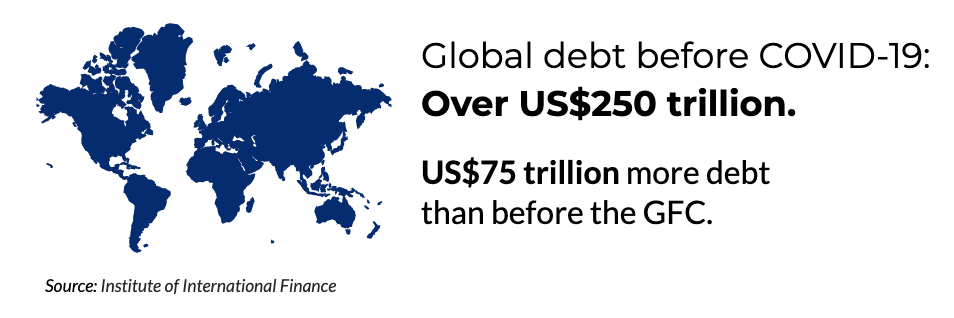

Realistically, the debt issue is not unique to Australia.

Before COVID-19 hit, global debt levels totalled over US$250 trillion (around A$350 trillion). It’s an extra $75 trillion deficit compared to the world’s total debt ahead of the global financial crisis (GFC).

Speaking to the economic impact of this issue, Credit Intelligence (ASX:CI1) Managing Director Jimmie Wong said investors should be on the lookout for secure investments in a credit crisis.

“If the Australian economy cannot recover fully in the next one to two years, more people will lose their jobs and there will be a [decrease] in exports to China and other markets … there will be financial trouble for many people,” he stated.

Now, as the pandemic leads companies and individuals to take on more arrears, signs point to a credit explosion and subsequent crash.

Deferrals and lending on the rise

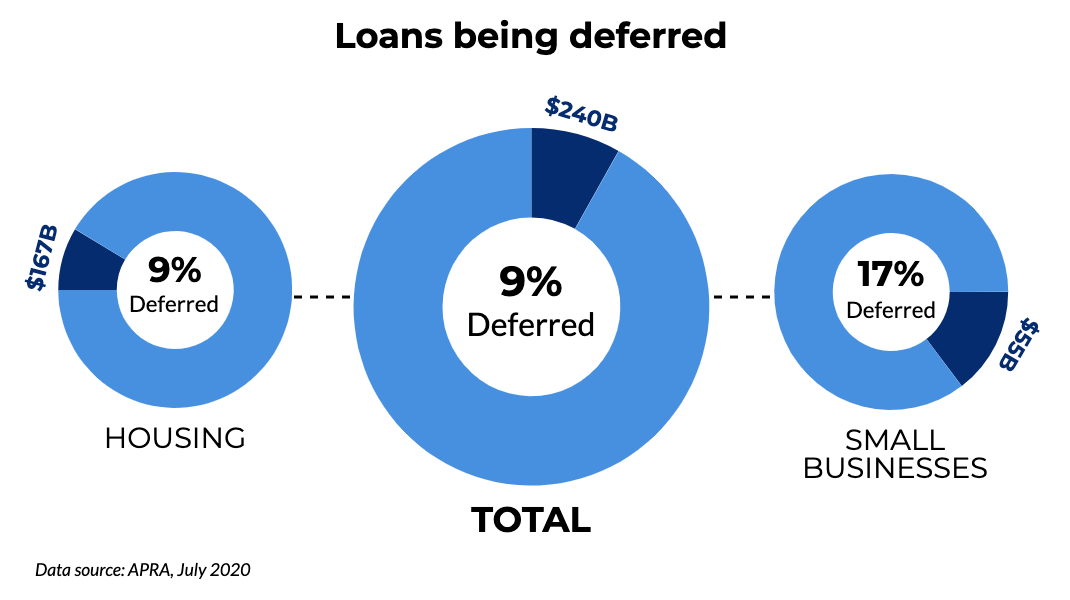

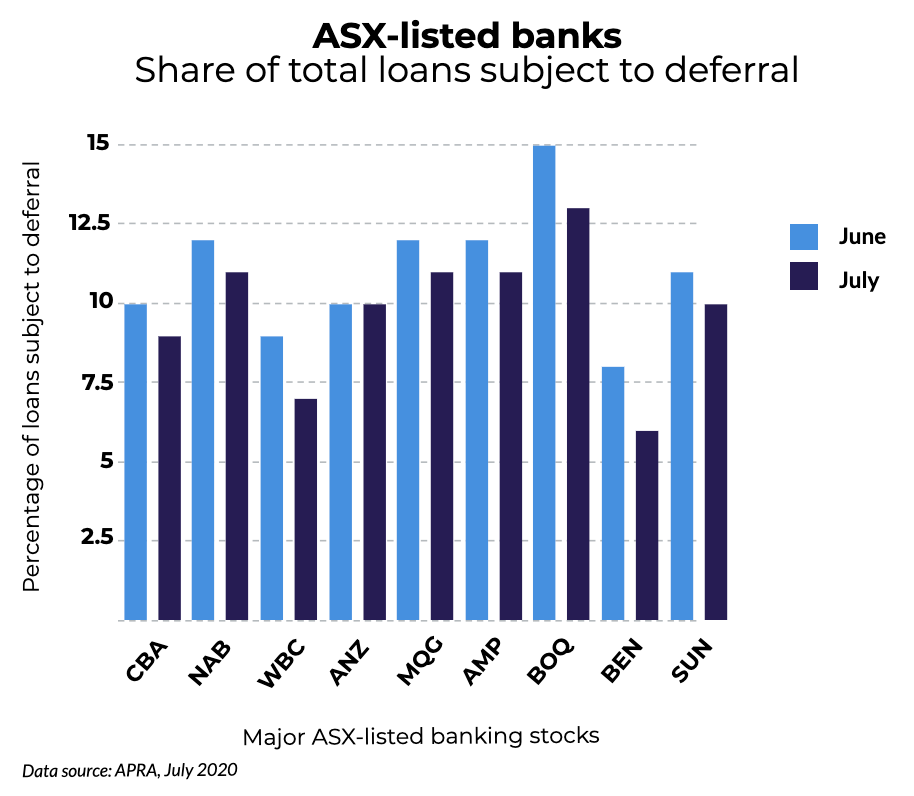

In addition to our current debt, there are other markers which point to a lending crunch. As homeowners and small businesses battle with the economic effects of the pandemic, loan deferrals are on the rise.

By the end of July, the Australian Prudential Regulation Authority (APRA) reported roughly nine per cent of all loan payments had been put on ice.

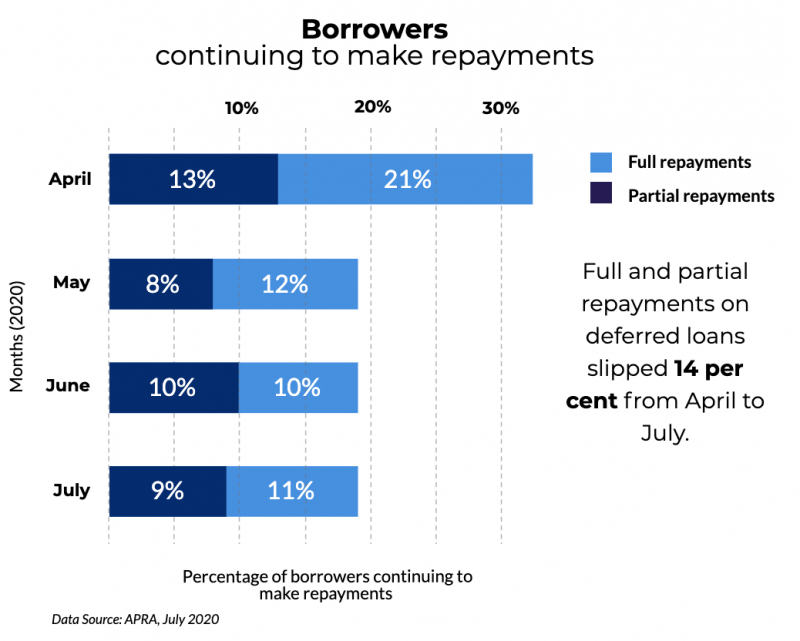

While those loans are deferred, the percentage of borrowers who continue to make partial or full repayments has slipped. Back in April, 34 per cent of debtors who’d deferred were still paying back their loans. Come July, that figure had slipped to just 20 per cent.

And while debt levels are already high, that hasn’t prevented the level of home loan commitments from rising.

In July, the Australian Bureau of Statistics (ABS) reported the sharpest-ever monthly rise in home loan lending. Over the winter month, the value of new home loan commitments skyrocketed 8.9 per cent, while personal lending also shot up by 6.9 per cent.

As Australians defer and sign up to more debt, it becomes increasingly clear that this economic downturn is following old patterns.

A familiar pattern

This won’t be the first credit bubble to burst down under. In fact, it bears striking similarities to historical deficits.

If we look at the fallout from the 2008 crash, the statistics paint a grim picture.

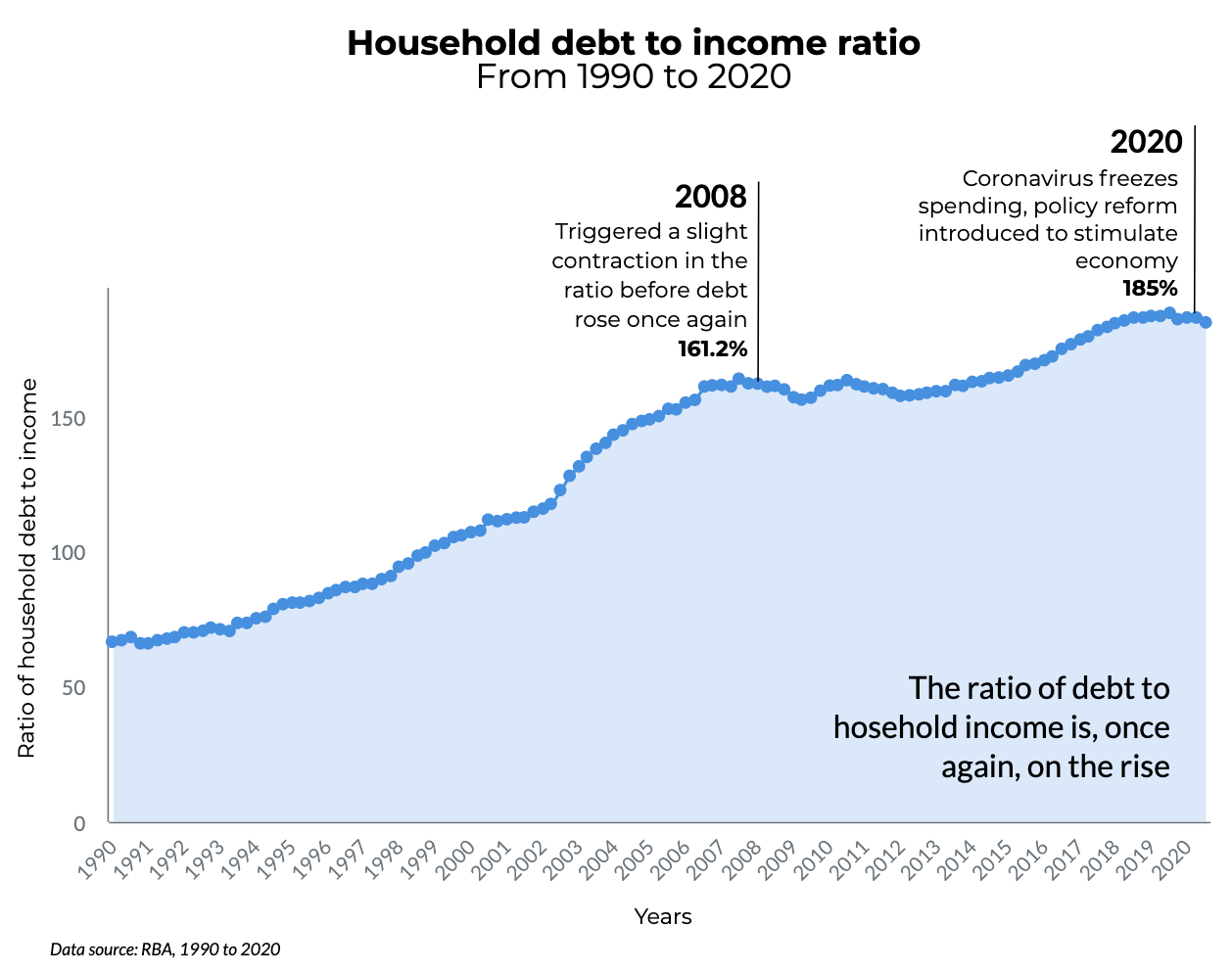

Back in 2008, Australia’s household debt to income ratio was at a staggering 161.2 per cent. That means if a person was earning $80,000 a year, their average annual debt totalled $129,600.

As the credit crash hit down under, the debt to household income ratio contracted slightly as bankers pressed pause on lending activity.

Since then, however, the ratio has been back on the rise, coming in at 185 per cent in June 2020.

There’s another historical similarity to 2008. Like now, home loans soared in the moments before the GFC. As the RBA explains it, investors and households took on more borrowings to purchase more assets — magnifying both their potential profit and potential losses.

However, when the bubble burst and house prices began to fall, this left banks and investors with major losses because they had borrowed so much.

A key catalyst for the burst was a lack of regulation for lending and mortgage-backed security (MBS) products. This meant many borrowers were handed out loans so large that they would be unlikely to be able to repay them, but it also meant fraud was common; borrowers would overstate their income and sellers would lie about the safety of the MBS product.

This meant when the crisis started to unfold, central banks and governments were overloaded by unexpected amounts of bad loans which were given out during the prior period of economic boom.

The recent relaxing of credit laws mean the Australian financial environment is ripe with risk for similar practices once more.

Who will fare the worst?

As a wave of fresh debt hits home, our once-stoic banks will be hit hard. In fact, when the rate of bad debt skyrockets, it’ll be enough to force some lenders to shut up shop.

Major, publicly listed banks will most likely escape the least scathed, but the impact won’t go unfelt among smaller, more competitive lenders.

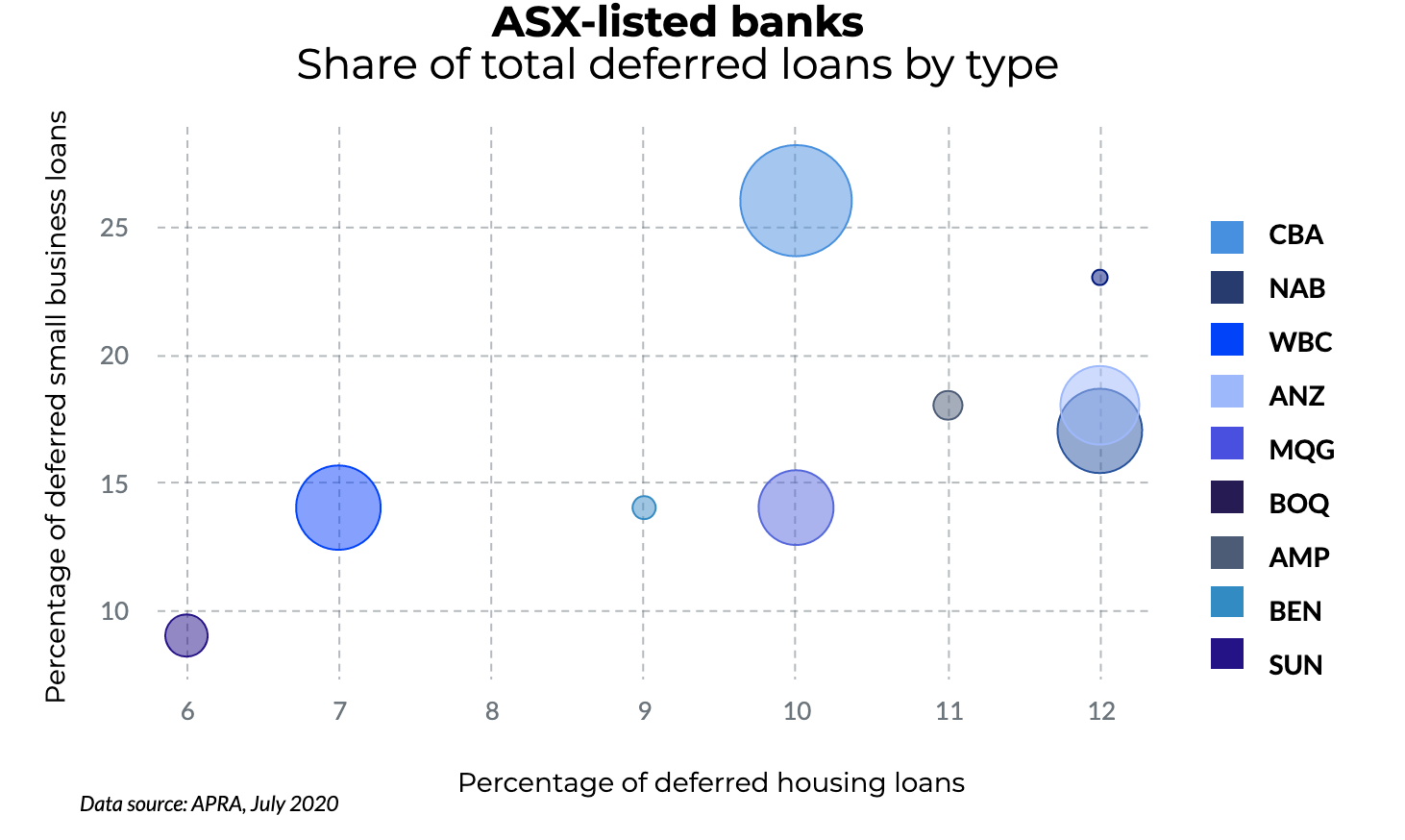

And while it’s considered a heavyweight authorised deposit-taking institution (ADI), Bank of Queensland (ASX:BOQ) has some decent risk exposure.

As seen in the bubble plot above, 12 per cent of the bank’s home loans and 23 per cent of its small business advances have been deferred. BOQ also carries a comparatively smaller market capitalisation — weighing in at $2.68 billion — meaning it’s got less of a safety net to handle prospective defaults.

On Tuesday, the lender announced a $175 million loan impairment would appear on its FY20 report. $133 million of that links to COVID-19 impairments — a thirteen-fold increase on BOQ’s first-half estimates.

Meanwhile, neobanks and fintech darlings will also feel the crunch.

BNPL giants like Afterpay (ASX:APT) and Zip Co (ASX:Z1P), which already contend with deepening consumer debt and operate at a loss, will feel the pinch when customers are unable to pay.

Others like Wisr (ASX:WZR), which offers low-interest personal loans based on strong credit ratings, will also struggle to ensure their model is accessible to a wider market if defaults and deferrals become the norm.

More broadly, hits to the financials sector will also impact mum and dad investors whose super is tied up in the stocks. When loans go bad, dividend payments will freeze and add extra financial strain. Collectively, because the big four banks are a substantial pillar of the Australian market, this phenomenon will be widely felt.

Nevertheless, there are still some ASX-listers who will find opportunity amid the crunch.

Who will benefit?

Of course, debt managers will be on the move as credit defaults abound. But this industry is fraught with complications.

Stock analyst Tim Boreham describes the credit crunch as a catch 22 situation — managers can work against a miserable market and rising defaults … “But too much misery and the ‘blood from a stone’ rule kicks in: delinquent loan books are only worth something if enough can be squeezed from the debtors to make the recovery worthwhile.”

Issues like this have seen small-cap managers like Collection House (ASX:CLH) and Pioneer Credit (ASX:PNC) grapple with their own re-capitalisation plans. And while it still managed to swing green in FY20, COVID-19 impacts shaved roughly $50 million from industry leady Credit Corp’s (ASX:CCP) profit margins over the year.

One company which seems prepared to weather the storm, however, is ASX-listed Credit Intelligence (ASX:CI1). The company has minimal exposure to the Australian market but recently acquired Sydney-based debt services business Chapter Two Holdings. While the buy is yet to impact CI1’s balance sheet, it’s set it up to make moves in the debt management space down under.

“Some industries will perform better in a bad economy, including Credit Intelligence, because we [have been] a debt management company for many years … we see a lot of room for expansion in Hong Kong, Australia and other countries as well,” said Credit Intelligence Managing Director Jimmie Wong.

Looking beyond the debt management space, players like FSA Group (ASX:FSA) could also grow amid a credit crunch.

The financials stock acts as the middle man, helping debtors create payment plans with their creditors. As the economic environment causes more borrowers to consider this option, FSA is poised to flourish.

In addition, businesses like QuickFee (ASX:QFE), which bridge the gap between corporate payers and payees, could also soar. The eCommerce stock provides flexible payment solutions for business clientele while ensuring companies get paid on time.

While it does fall into the BNPL category, what makes QFE different is its target market: it’s focussed on the professional services industry, a broad market which grew its total revenue by 10.6 per cent over 2019.

And tech stock IODM (ASX:IOD) could also come to the fore with its credit management software. As the focus turns to managing debt parcels, a tech-centric solution could gain popularity among investors.

The bottom line

Regardless of the winners and losers in this latest credit crisis, it’s clear consumers will face the ultimate struggle.

Ballooning debt — both at a Federal and household level — poses serious risks. And Karen Cox, CEO of the Financial Rights Legal Centre, says it has lasting implications.

“Unsustainable debt hurts real people and is a short-sighted fix for a flailing economy.”

Financial Rights Legal Centre CEO, Karen Cox

Just how the great Australian credit crisis plays out remains to be seen.

If you or someone you know is experiencing financial difficulty, help is available. Contact the National Debt Helpline on 1800 007 007.