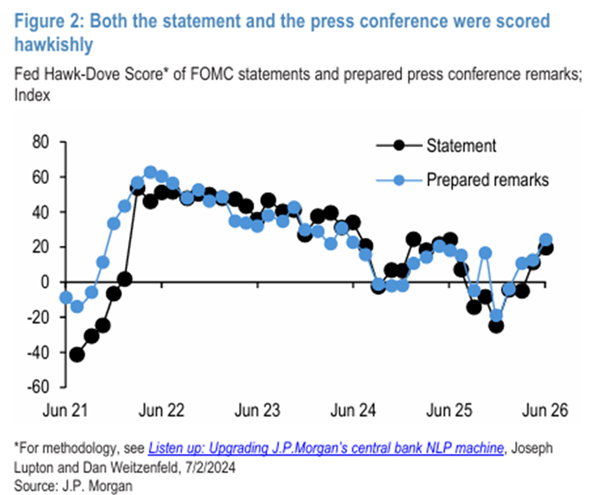

JPM scored Kevin Warsh’s first FOMC as one of the most hawkish events of this cycle — both the statement and the prepared press conference remarks landed clearly on the hawkish side of their hawk-dove index. The tape didn’t show it. The S&P leaked, the Dow held, gold ripped, and oil collapsed.

Listen to the HotCopper podcast for in-depth discussions and insights on all the biggest headlines from throughout the week. On Spotify, Apple, and more.

Two macro shocks layered on top of each other this week. Iran/Israel de-escalation crushed crude and dragged Energy sharply lower. Warsh’s debut tightened financial conditions across long-duration assets.

The two reactions partially cancelled at the index level — and the market is now underpricing how decisively hawkish this Fed actually is.

The Powell-Era Fed vs. the Warsh Fed

Powell opened press conferences with “Good afternoon” or “Hello everyone.” Warsh opened with “Good day.” Small touch, but markets immediately read it as a signal. The Powell openers were familiar and market-friendly; “Good day” is a Greenspan-era cadence. The tone of the regime was set before Warsh said anything substantive.

The hawk-dove read above tells the story numerically. Here is what stood out qualitatively:

- Statement cut from 341 to 130 words. Greenspan-length. Less language means fewer pre-commitments, more optionality, and a Fed that reserves the right to surprise.

- No forward guidance. The Powell era’s signature instrument was simply not offered. Risk assets can no longer underwrite policy visibility into multiples.

- Hawkish dot plot. Nine of eighteen members now project hikes by year-end. The 2026 median dot moved up 35bp to 3.75%. Seventeen of eighteen flagged inflation risks as skewed to the upside.

- OIS prices a full hike by the October FOMC and more than 45bp of additional tightening by spring. Front-end yields jumped, real yields rose, breakevens fell.

- Warsh did not submit his own dot. The SEP normally has nineteen participants — seven governors and twelve regional Fed presidents. This time it had eighteen. Markets noted the absence: Warsh should have been the nineteenth, but he wasn’t. There is no “Warsh dot” to pre-trade because there isn’t one.

The five task forces: What Warsh wants to change

Warsh used his first meeting to announce five internal task forces. The message is unmistakable — he wants something to change, and these are the five frontlines:

- Communications. The most consequential of the five. The shortened statement and missing forward guidance signal where this is going: less talking, and possibly retracting the dot plot itself — an instrument markets treat as a forward contract on Fed intent. Warsh’s own missing dot was the first trial balloon.

- Balance sheet. Warsh is notorious for wanting QT. He has long argued the Fed’s balance sheet runs structurally too hot. Expect bias to lean tighter — QT pace, SRF, RRP, and the long-run SOMA portfolio all back in play.

- Data sources. A review of which inputs drive policy. Payrolls, CPI, PCE, and surveys may be deprioritised in favour of higher-frequency or alternative measures. Pre-trading specific data prints just got harder.

- Productivity and AI. Whether AI is genuinely lifting potential output is being formally integrated into the framework. A Fed that internalises higher trend productivity is a Fed that can run tighter without breaking the economy — and is less inclined to ease into wobbles.

- Inflation frameworks. Possibly the most important. Core PCE is on the table for revision toward trimmed-mean and alternative anchors that strip out tail moves. A trimmed-mean anchor is structurally harder to dovishly explain away — and the seventeen-of-eighteen upside-skew dots reinforce that this is where Warsh wants the framework to land.

Bottom line: policy now arrives with less notice, less guidance, and an asymmetric hawkish tilt. The institutional plumbing of the prior regime is all under review. Long-duration multiples lose the visibility premium they had under Powell.

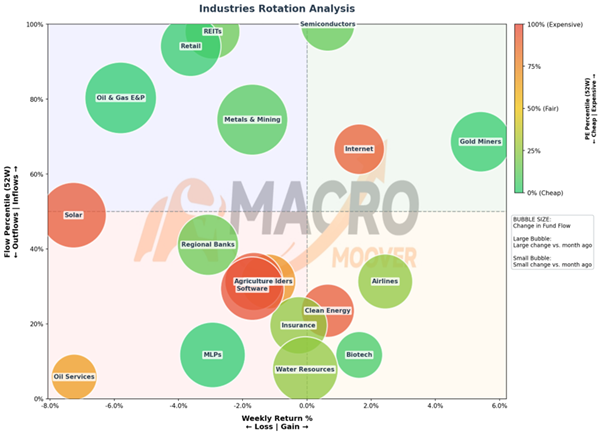

The rotation: A quiet confirmation

The flow data is doing exactly what a Warsh-Doctrine Fed would push it to do. Capital is rotating out of long-duration growth and into front-end-friendly cyclicals — financials, industrials, and materials hold the upper-right conviction quadrant at or near peak flow percentile, while rate-sensitive longs and traditional defensives sit in the duration-victim zone. The character of the move is the tell: orderly, deliberate, dispersion-led rather than panic-led. Institutions are not running for safety. They are repricing the long-run policy function and rebuilding positioning under it.

The clearest beneficiaries are names where cash flow is near-term and rate-sensitive. Financials (XLF) sits in the conviction quadrant — a steeper curve and a Fed less inclined to subsidize duration support net interest margin and asset-sensitive earnings. JPMorgan (JPM), Bank of America (BAC), and Goldman Sachs (GS) anchor the move. Industrials (XLI) and Materials (XLB) capture the real-economy bid that aligns with the supply-side AI/productivity narrative being formalized into the Fed’s framework — Caterpillar (CAT), Eaton (ETN), Linde (LIN), and Nucor (NUE) all sit in the same accumulation cohort, with Industrials in particular moving from near the absolute floor of flows a month ago to the maximum reading possible this week.

Two flow callouts stand out. Gold Miners (GDX) posted the strongest weekly return on the entire industry board, with flows accelerating into the upper quartile — the rare environment where gold rallies even as real yields rise, paid for by an inflation framework the Fed itself is signaling concern about. Solar (TAN) is the inverse: peak inflows a month ago combined with one of the deepest weekly drawdowns — the textbook duration-victim profile that the Warsh Doctrine punishes most directly. The Iran-driven move in Energy sits separately — a geopolitical risk-premium reset, not part of the Fed trade.

SpaceX (SPCX) is the first casualty of the new regime. After soaring from its $135 IPO price to $225, shares have already fallen back to ~$192 as retail enthusiasm fades. The biggest long-duration listing in history launched the same week the Fed signalled less support for stretched valuations.

The same risk extends to Rocket Lab (RKLB) and the AI-memory trade (MU, SK Hynix, Samsung): the cycle may remain intact, but the Fed tailwind has disappeared.

Real Estate (XLRE) remains the clearest rate victim. Despite strong inflows, returns have rolled over, while PLD, AMT, and EQIX still look vulnerable to further positioning unwinds.

The market did not yet read the FOMC as decisively hawkish — the Iran shock muddied the tape. The flow data is less ambiguous.

The Warsh Doctrine has begun, and capital is already adjusting.

Join the discussion: See what’s trending right now on HotCopper, Australia’s largest stock forum, and be part of the conversations that move the markets.

The material provided in this article is for information only and should not be treated as investment advice. Viewers are encouraged to conduct their own research and consult with a certified financial advisor before making any investment decisions. For full disclaimer information, please click here.