It’s our first week after the US Federal Reserve’s Jerome Powell cut US interest rates by -50bps, but on HotCopper, there were some spots of bad news.

Pain points for HotCopper

First, HotCopper users focused a lot of chagrin towards Canberra this week as smallcap darling BPH Energy saw an attempt to ‘unfreeze’ its flagship PEP-11 oil and gas licence offshore NSW rejected by Federal Industry Minister Ed Husic.

Elsewhere, shareholders of embattled Star Entertainment wondered what the company’s -43% drop on Friday would mean for investors in the long-term. But there were bright points, too: lithium junior Raiden Resources’ news it will kick off long-awaited drilling this weekend led to a surge of optimism among long-time holders and market watchers alike.

China outshines US Fed

Outside of HotCopper in the wider world of markets, it was a China-heavy week this week.

On Tuesday, the Red Dragon’s government announced further stimulus measures for the world’s struggling second largest economy – more mortgage easing, further interest rate cuts, and something we haven’t seen this year: the Chinese central bank will give money to brokers in the country to buy Chinese stocks en-masse.

While China has been announcing stimulus measures all year to no real effect, in the context of a world where the Fed cut rates last week, it appears this time risk-on sentiment has come to roost.

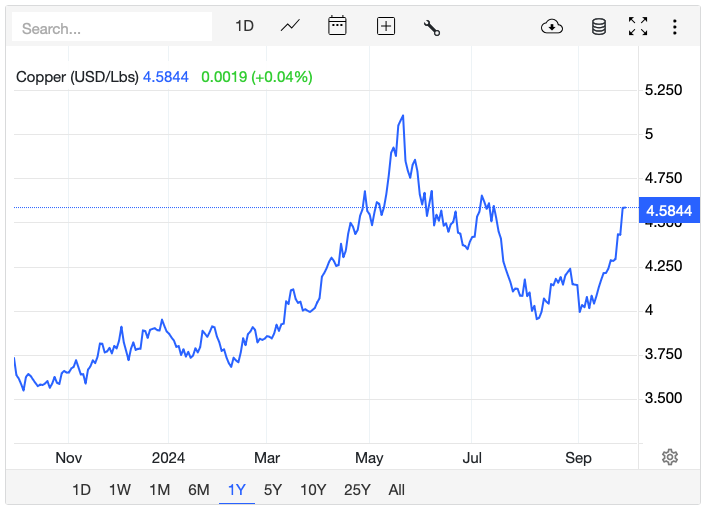

Just look at metals prices: aluminum was up nearly +6% Week on Week (WoW); zinc jumped over +7.5% WoW and copper jumped +7% WoW as traders bet this batch of stimulus will be enough to turn around the lagging ship that has been China’s economy since COVID-era lockdowns were lifted (following historic riots in early 2023.)

Stimmy not without skepticism

How long can this latest stimulus afterglow last? Time will tell.

It’s worth noting that alongside renewed tension in the Middle East – Israel and Lebanon appear set for their own war – China’s news helped push Brent Crude prices to US$75/bbl.

But by Friday, that price had subsided back towards US$71.00/bbl – a decline driven, in part, by skepticism towards whether China’s latest stimulus is enough to boost oil demand broadly in the world’s second largest economy.

Australia’s big miners were beneficiaries of the rise in commodities – including iron ore prices in Singapore which, on Friday afternoon, were up to US$102/tn. But don’t forget Chinese state-owned media only a few weeks ago described a US$100/tn iron ore price as “irrational.”

Rebates complicate local CPI

Talking of Australia, in the land down under, inflation continues to track downwards. In fact, monthly CPI on a year-by-year basis was 2.7% in August 2024 – a steep drop from July where the read was higher at 3.5%. But that steep drop was driven in large part by energy rebates coming from the Federal government, complicating the numbers somewhat.

It will be interesting to see what CPI numbers do across the next few releases; the next more-in-depth quarterly data is released towards the end of October. Surprising nobody, the RBA also kept rates on hold this week at 4.35%.

So what else happened this week?

Odds & Ends: hydrogen, nuclear, dividends

There was more than enough to pay attention to. ASIC has been on another greenwashing push, stinging both Macquarie and Vanguard with the latter copping a fine near A$13M.

Overseas, the hydrogen narrative took another blow as Shell pulled out of its plans to build a hydrogen facility in Norway. Elsewhere, OpenAI said it would become a for-profit company – so-long to Altman’s NGO-style philosophy – and analysts at Macquarie reckon climate change is a threat to the value of Aussie bank stocks.

Elsewhere, a deal between Microsoft and another company called Constellation saw ASX-listed uranium stocks rocket as that deal is set to see the USA’s controversial Three Mile Island reactor facility brought back online.

The real story here is a synthesis of AI and nuclear – what if the latter powers the next round of breakthroughs? Berkshire Hathaway sold down its stake in Bank of America to 10.5%: an increasing number of US citizens are reporting jobs as “hard to get,” and the ACCC prolonged its decision on the long-awaited reverse listing of Chemist Warehouse into October.

Oh, and the ASX is in a dividend recession: payouts market-wide in Q2 of CY24 fell -19% YoY.

What were HotCopper users watching?

- Raiden Resources confirms long-awaited drilling to kick off at Andover, WA this weekend

- HotCopper users digest news BPH Energy’s PEP-11 NSW permit ‘unfreeze’ knocked back

- Star Entertainment shareholders discuss what Star’s financial woes mean for investors

Australian Economy

- Oz inflation comes in at 2.7% MoM vs 3.5% pcp as energy rebates distort downward

- RBA leaves rates on hold at 4.35% with housing upside pressure expected

- Oz traders scale back hopes for RBA cut this year amidst constant warnings it won’t happen

Australian Equities

- Dividend payouts market-wide in Q2 CY24 fell -19% YoY: Janus Henderson

- Cettire soars back above $2/sh following auditor greenlight on bad-press-hit company

- Coles and Woolworths hit with ACCC lawsuit alleging misleading conduct

- ACCC prolongs Chemist Warehouse reverse listing decision til October

International Economies

- China’s central bank unveils economic stimulus measures – once again

- China’s central banks will provide funding to brokers to buy Chinese stocks

- Capital Economics says China’s latest stimulus measures fall short again

- OECD flags US GDP growth slowing in 2025

- Increasing number of Americans reporting jobs “hard to get”

International Equities

- Quantum Energy CEO says the US fracking revolution is over

- Visa stocks fall as the US launches an antitrust investigation

- Berkshire Hathaway has sold down its Bank of America stake to 10.5%

- Constellation Energy soars after Microsoft-backed nuclear power deal hits market

Commodities

- ASX uranium companies soar early week on Microsoft deal

- Gold climbs to US$2,630+ by Tuesday of Week 38; Friday sees US$2,670+

- Brent flirts with US$75/bbl early week as Israel-Lebanon war expands

Geopolitics

- Kamala Harris vows to increase USA’s critical minerals stockpile

- RBC Capital Markets say oil markets don’t reflect risk of full blown MidEast war

- OPEC’s latest oil outlook sees continued growth to 2050; net zero fantastical

Regulatory + Odds & Ends

- Macquarie fined $4.99M by ASIC for allowing clients to manipulate electricity futures

- Vanguard to pay $12.9M to ASIC for greenwashing over broad ESG index fund

- Shell abandons plans to build-out hydrogen plant in Norway; cites low demand

- Macquarie analysts warn climate change may hurt banks’ housing loan books

- OpenAI to become a for-profit entity

Join the discussion: See what’s trending right now on HotCopper, Australia’s largest stock forum, and be part of the conversations that move the markets.