Join our daily newsletter At The Bell to receive exclusive market insights

The U.S. indices kept grinding to fresh highs. Oil stayed elevated. The U.S.-Iran conflict delivered no new headline — no ceasefire, no escalation, no fresh pricing signal. The S&P 500, Dow Jones, and Russell finished inside a quarter point of flat at or near record levels. The Nasdaq eked out a gain, while Australian shares bucked the trend and declined. Gold held its bid, silver faded, Bitcoin idled.

Listen to the HotCopper podcast for in-depth discussions and insights on all the biggest headlines from throughout the week. On Spotify, Apple, and more.

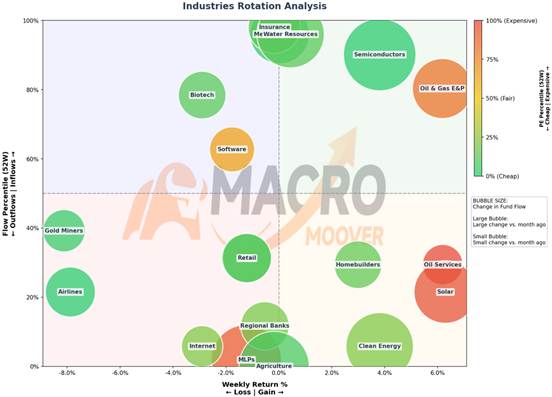

When the macro stops delivering catalysts, capital doesn’t sit — it reorganises. The answer to “where is capital going?” is not in the index. It’s in the bubbles.

The theme: Two engines drive the tape

The dominant force this week was the absence of one. U.S.-Iran headlines froze, oil held bid, and indices drifted to new highs on nothing but internal rotation — the late-cycle tell, benchmarks aloft while the composition churns.

Silicon is where conviction sits. The Philadelphia Semiconductor Index (SOX) is now on a 17-session run — the tape’s verdict on where money wants to be. With breadth this narrow and SOX carrying the indices, semis stop being a sector call and become the market’s default guidance.

Tesla and Intel bookended the week and confirmed the setup. Tesla reported into peak-flow, negative-return positioning in Discretionary; Intel into the board’s sharpest flow acceleration in Semis.

Neither caused the rotation — both validated it. Capital picked two lanes, oil and silicon. Everything else was pain, short-covering, or forced exit.

Energy: From logistics detour to physical supply cut

Oil’s quiet week is the loudest thing on the tape. Crude stayed bid, not on new headlines, but on the structural math the market is finally running.

The shock absorbers are gone. Saudi and UAE spare capacity is stranded behind a blockaded strait; U.S. shale can’t respond inside six months; Russia is producing less, not more. April inventories drew at one of the fastest paces on record — and still couldn’t close the gap.

The real story is on the ground in Iran. Under the U.S. naval blockade, the pumps keep running, but the barrels can’t leave — they’re piling into onshore storage with two to three weeks of runway left. The Treasury Secretary has been conspicuously public about it, warning Kharg Island will fill “in a matter of days.” When the tanks top, wells shut in. Iran’s fields are old, and industry consensus says several hundred thousand barrels a day of capacity could be lost for good.

That’s the pivot. Until now, the shock was logistical — rerouted, delayed, not destroyed.

The storage-top moment, expected late April, turns it physical and irreversible, stacking permanent loss onto a disruption already running in double-digit mbd.

A ceasefire doesn’t unwind it.

This is what the flow is pricing. Oil & Gas E&P carries the cleanest conviction signal on the industry board — EOG Resources (EOG), Diamondback Energy (FANG), and Occidental (OXY) absorbing the bid; Oil Services — Schlumberger (SLB), Halliburton (HAL), Baker Hughes (BKR) — re-rating alongside.

Large-cap cash machines Exxon Mobil (XOM), ConocoPhillips (COP), and Chevron (CVX) anchor the move. Aus names followed: Woodside (WDS) reversed early losses, and Santos (STO) climbed for the week.

Not a headline trade — a regime trade.

Semiconductors: Wanted, and validated

Flow blasted from the absolute floor a month ago to near the peak this week — the most dramatic acceleration on the industry board, paired with positive return and PE at zero. Textbook cheap-and-wanted.

Intel (INTC) delivered the quiet validator: Data Centre & AI growing at the strongest rate in years, AI PCs now the majority of client CPU mix, margins expanding, Q2 guide sustaining momentum. The AI CPU comeback is in the numbers, not just the narrative — Foundry remains the long-term hinge. NVIDIA (NVDA), Broadcom (AVGO), and ASML (ASML) lead alongside INTC.

When flow, price, valuation, and fundamentals align like this, you stop calling it a trade. Full breakdown: Intel Q1 deep-dive here.

The rest: Flat or painful

Consumer Discretionary sits in the most dangerous quadrant — flow at the maximum, worst return in the cohort. Tesla (TSLA) reported into that exact setup: auto revenue beat, FSD scaled, but energy storage contracted, and Musk signalled a 2026 CapEx step-up. This tape is not ready to underwrite. (Full breakdown: Tesla Q1 deep-dive here.)

Staples — Costco (COST), Walmart (WMT), PepsiCo (PEP) — held the bid where fundamentals support it; Utilities, REITs, and Health Care got no such treatment. Industrials collapsed from near-max flow a month ago to zero as the AI-capex industrial narrative gets deprioritised for direct oil-and-silicon exposure.

Homebuilders (DHI, LEN) quietly accumulate ahead of a rate regime that favours real-economy names. Solar, Clean Energy, Airlines, and Gold Miners were either short-covering bounces or forced-liquidation stories — don’t chase.

New highs. High oil. Tehran quiet. SOX at 17 straight. When the market loses external catalysts, it tells you where conviction lives through flow.

This week, the lights are on in two rooms: The oil complex pricing in a physical supply regime, and silicon pricing in the AI cycle’s next leg. Smart money has already picked its lane — the only question is which room you’re in.

Join the discussion. See what’s trending right now on Australia’s largest stock forum and be part of the conversations that move the markets.

The material provided in this article is for information only and should not be treated as investment advice. Viewers are encouraged to conduct their own research and consult with a certified financial advisor before making any investment decisions. For full disclaimer information, please click here.

General ETF disclosure: Before investing in an ETF, you should read both its summary prospectus and its full prospectus, which provide detailed information on the ETF’s investment objective, principal investment strategies, risks, costs, and historical performance (if any). You can find prospectuses on the websites of the financial firms that sponsor a particular ETF, as well as through your broker. Investment returns will fluctuate and are subject to market volatility, so that an investor’s shares, when redeemed or sold, may be worth more or less than their original cost. ETFs are subject to market volatility and the risks of their underlying securities, which may include the risks associated with investing in smaller companies, international securities, commodities, fixed income, and more. An ETF may trade at a premium or discount to its net asset value (NAV).