For investors looking to achieve inflation-linked absolute returns, the infrastructure asset class provides a number of attractive characteristics. Over the past 10 years, infrastructure has emerged as a stand-alone asset class, and many large institutions have made sizeable allocations within their portfolios.

For the most part, allocations to infrastructure have been directed toward private market transactions and unlisted infrastructure funds, with the aim of achieving stable long-term, inflation-linked returns. Over the past five years, the weight of funds flowing into this relatively young asset class has grown dramatically. This increasing demand for unlisted infrastructure assets has not been met by an equivalent increase in the supply of suitable infrastructure opportunities. According to Preqin, 2019 saw a total of $98 billion raised from investors through 88 fund closures (including the two largest infrastructure funds ever closed).1 Dry powder at the end of 2019 was $212 billion, which is more than double the figure at the end of 2015.

At the start of 2020, there were 253 funds reported in the market, targeting more than $200 billion. This dynamic of growing demand and constrained supply, combined with stimulatory monetary settings, has exerted significant downward pressure on available returns in unlisted infrastructure and capital deployment in unlisted infrastructure has become increasingly challenging.

The listed infrastructure market, however, provides investors with a broad, deep and liquid range of infrastructure investment opportunities. As a result, listed infrastructure is an alternative option for capital deployment in this asset class. It also provides the investor with flexibility to choose or amend an investment horizon.

The Infrastructure Opportunity Set

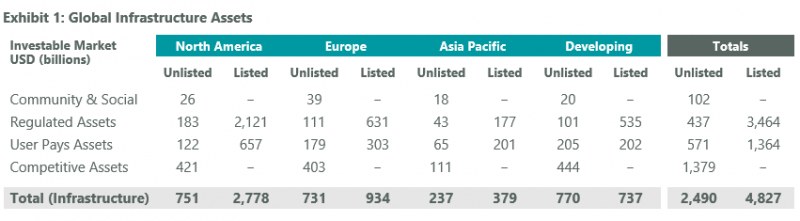

The infrastructure opportunity set is large. Depending on how broadly infrastructure is defined, there are $20–$50 trillion of infrastructure assets globally. Most of these assets are under public ownership and therefore not available to private investors. We estimate that, on a narrow definition, roughly $7 trillion of global infrastructure assets are privately owned, of which listed infrastructure accounts for 70% or $5 trillion of asset value (approximately $2.5 trillion of equity value).

There is sound evidence that the investable universes for listed and unlisted infrastructure are not substitutes. First, they offer different subsector exposures (Exhibit 1):

- Community and social assets, such as schools, universities, hospitals and government facilities that help deliver social services.

- Regulated assets, such as water, electricity and gas transmission and distribution, for which a regulator determines the revenue a company should earn on its assets.

- User pays assets, such as rail, airports, roads and telecommunications towers, which move people, goods and services throughout an economy and where pricing, volume and revenue are determined by how many people use the assets.

- Competitive assets, such as telecommunication and utility retailers.

Some assets, such as community and social assets and competitive assets, are available only in the private, unlisted market. The listed infrastructure market, however, provides much more depth in regulated utilities and user pays assets — high-quality core infrastructure assets that are more liquid.

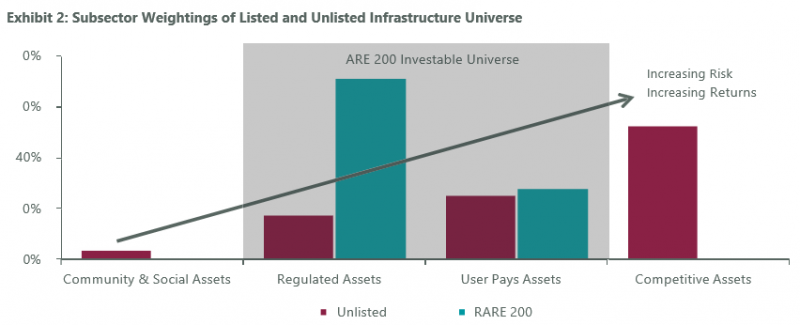

Second, our assessment of the infrastructure asset class shows there are also meaningful differences in risk exposures for the listed and unlisted universes, which can lead to different observed performance (Exhibit 2). This suggests these universes are not substitutes; rather, they are complementary. Different subsector and risk exposures allow investors in both listed and unlisted infrastructure the opportunity to improve portfolio construction efficiency and control unintended portfolio biases or risks.

Regulation Underpins Long-Term Returns While Allowing for Opportunistic Return Enhancement

Whether an infrastructure investment is held in a listed or unlisted form, the key driver of asset-level risk and returns is regulation. The returns “allowed” by the regulator are a critical driver of long-term asset-level returns and the operating conditions or constraints imposed by the regulator are key ongoing risks to be managed or mitigated.

Case Study: UK Water

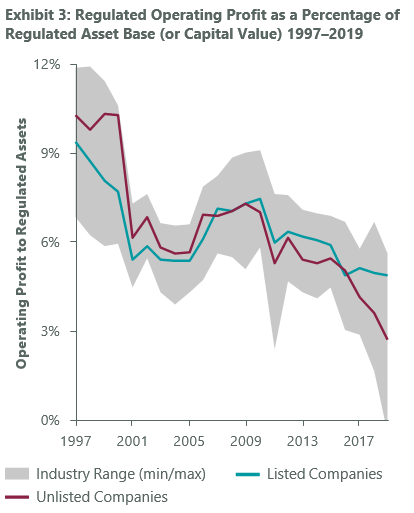

Listed and unlisted UK water companies share the same regulation and similar macroeconomic drivers, and regulatory allowed return on capital is the main driver to returns in this subsector. While there is scope to outperform the allowed return through operational skill, for the 2001–18 period the difference in operating profit (as a percentage of the regulated asset base) of the average listed and unlisted company was less than 1%.

UK water companies are regulated based on five- year periods, and it can be observed from Exhibit 3 that for the 2001–05, 2006–10 and 2011–15 regulatory periods the regulator (the Water Services Regulation Authority, or Ofwat) followed policies that resulted in a relatively narrow range of return outcomes across the industry. A deliberate change occurred in the 2016–20 regulatory period as the UK water industry regulatory policies intended to reward better-run companies. Regulators are now agreeing on a series of operational and customer engagement benchmarks with companies and attaching financial penalties or incentives to the outcomes.

Listed companies have a range of tools to remunerate management, for example, allowing some companies to strive for improved execution and achieve better returns. This indicates an opportunity for active infrastructure investors to allocate to the better performers.

The average return on regulated assets (or, as described by the regulator, regulated capital value) has shown relative consistency over the long term, although in the past few years the returns allowed by the regulator (assessed on a weighted average cost of capital approach) and achieved by the companies have come down, largely as a function of the yield environment, as bond yields have compressed.

Return on equity (ROE), as reported by the companies, and the return to equity holders (investors) are a function of the operating returns (outlined above in Exhibit 3) and the capital structure and financing of the companies. The capital structure of many of the unlisted water companies reflects significantly higher debt and leverage than the listed water companies. For the unlisted companies, this may result in higher returns, but also higher volatility and greater financial risk.

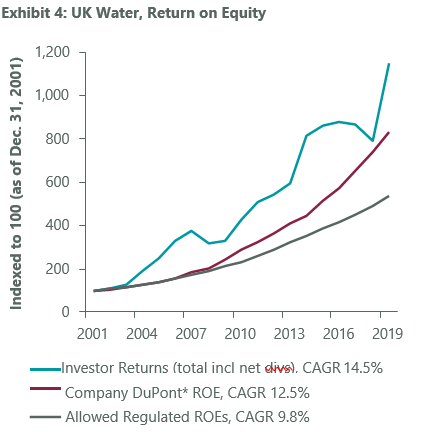

Over the long term, the returns to equity holders reference the ROE reported by the companies and the ROE2 allowed by the regulator. Exhibit 4 indexes the allowed ROE, reported ROE and investor returns (income and capital) for the listed UK water companies for the 2001–19 period. The compounded company- reported ROE3 has exceeded the regulator-allowed ROE by approximately 270 basis points per annum, indicating that the companies are outperforming the regulator’s operating assumptions and agreed business cases. It is common around the world for regulators of essential service companies to set return benchmarks that the companies subsequently outperform. This is generally achieved through operational and/or financing efficiencies and promotes long-term benefits for both companies and their investors and ratepayers, their customers. Returns to equity holders (investors) over the period have exceeded company-reported ROE by a further 200 basis point per annum, likely because of the:

- Market’s view of the company’s cost of capital being lower than that allowed by the regulator (noting that most of the investor return outperformance has occurred during 2019); and

- Significant merger and acquisition (M&A) activity in the sector, given that 10 companies were privatised by way of initial public offering in 1990 and today only three remain (during the 2001–19 time period there were six successful M&A transactions and one unsuccessful transaction, all with deal values greater than GBP1 billion).

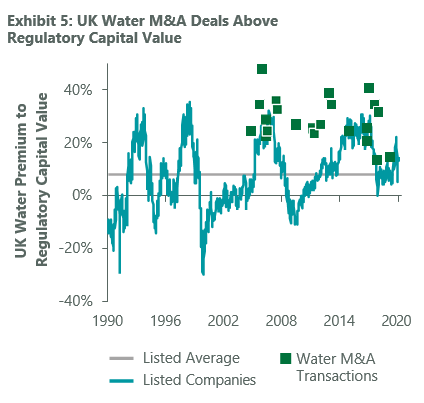

In the past 10 years, listed UK water companies have traded from a 5% discount to as much as a 25% premium to their regulated asset base, while private transactions have mostly occurred closer to a 30% premium to asset base. This has created opportunities for listed market investors to gain exposure to the UK water sector at (often) significantly more attractive entry prices.

With lower valuations for listed UK water companies and private acquisitions of these companies occurring at upwards of a 30% premium to asset base, we believe the two most likely outcomes for long-term holders of listed UK water companies are:

- The company performs broadly in line with its peers and given their lower entry price, investors earn a higher return on their investment than they would have with similar unlisted UK water companies.

- The company is taken private by an unlisted fund at an attractive exit valuation. There has been

Either way, over the long term, our analysis indicates holders of the listed stock are likely to generate better risk/return outcomes than their unlisted counterparts. This is almost entirely the result of the more favorable entry price.

UK water infrastructure illustrates the complementarity of listed and unlisted infrastructure universes. Despite the underlying assets of listed and unlisted companies being close substitutes, there can remain a wide range of returns and large discrepancies in valuation, both between listed and unlisted companies and within each group. This suggests conditions are in place to use listed infrastructure investments opportunistically for return enhancement while maintaining a similar exposure to the underlying assets.

Case Study: North American Electric Utilities

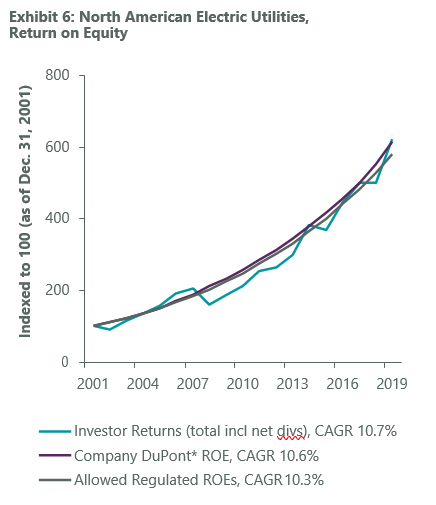

North American electric utilities are regulated on a state-by-state basis but generally use a nominal allowed ROE approach. While there is generally no set regulatory period, either the company can initiate a regulatory review (if it is under-earning its allowed ROE) or the regulator can initiate a review (if it believes the company is over-earning). This regulatory regime, therefore, creates a direct relationship between the regulator-allowed ROE and the returns to equity holders of the companies.

Exhibit 6 indexes the allowed ROE, reported ROE and investor returns (income and capital) for 42 listed North American electric companies for the period 2001–19. The compounded company-reported ROE has exceeded the regulator-allowed ROE by approximately 30 basis points per annum, indicating that the companies are outperforming the regulators’ operating assumptions and agreed business cases (as is normal for many regulated utilities).

Returns to equity holders over the period have further exceeded company-reported ROE by an additional 10 basis points per annum on average. The range of returns to equity holders versus the allowed and reported ROEs among the companies in the study in any given year is significant. This again illustrates that while regulation underpins long-term returns, liquidity allows listed infrastructure investors the ability to enhance infrastructure returns.

Listed Infrastructure Achieves Similar Returns but with More Flexibility

It is not surprising that asset-level returns are similar for listed and unlisted infrastructure and heavily reliant on the returns allowed by regulators, given that the holding structure should not materially affect the cash flows at the asset level. However, investors are chiefly concerned with the achieved returns from their investment, rather than the asset-level returns. How comparable are the long-term achieved returns for investors in listed and unlisted infrastructure?

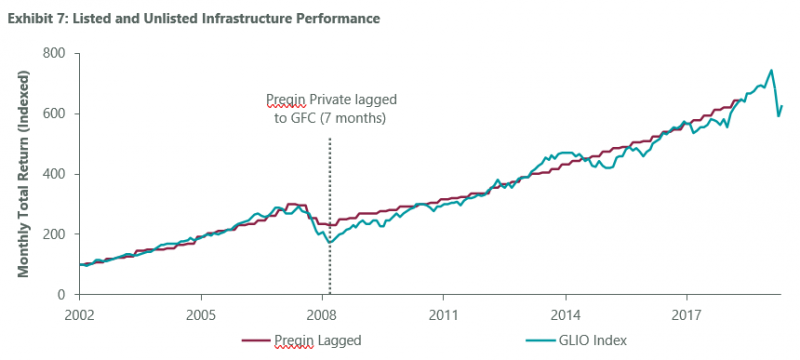

In order to evaluate this, we compared returns

for the PrEQIn Infrastructure Index (a proxy for unlisted infrastructure funds)

with returns for a broad global listed infrastructure index maintained by the

Global Listed Infrastructure Organisation (GLIO) (Exhibit 7).

We offer several observations on Exhibit 7:

- While there is no material difference in returns over most medium to long-term time periods, listed infrastructure clearly demonstrates the trade-off between liquidity and volatility.

- There can be a significant valuation lag between the listed and unlisted markets. It is evident that through the Global Financial Crisis (GFC) in 2008, the unlisted funds continued to write-up the value of their assets. During this time the listed market had already corrected significantly. Valuations in the unlisted market only started to be reduced in late 2008/early 2009. We note that in 2009 there was a significant drop in transactions (not pictured here), approximately 40%, likely due to the divergence between the price expectations of sellers and buyers. For this reason, the GLIO Index lags the results from the PrEQIn Index by seven months (estimated to be the average “valuation lag”).

- Listed infrastructure had very strong returns following the GFC correction, reflecting that the assets were undervalued during this period. Given the underlying cash flows of the infrastructure assets did not materially change, the listed infrastructure assets recovered all of their losses within three years and continued to perform strongly after that.

- Listed infrastructure asset prices rose in late 2014 and early 2015 on the back of ongoing monetary stimulus and overly optimistic valuations in the U.S. pipeline sector in particular. This mispricing corrected somewhat in late 2015.

Conclusion

We believe to take advantage of the infrastructure opportunity investors require a detailed understanding of the underlying assets. Focusing on underlying assets in listed infrastructure markets allows investors to capture opportunities that arise when equity markets misprice infrastructure assets due to a focus on short-term information. Meanwhile, regulation and contractual structures underpin the cash flows and determine long-term outcomes.

Listed infrastructure offers a broad and deep investment universe of high-quality infrastructure stocks and a complement to unlisted infrastructure for capital deployment in this asset class. Investors prioritising the flexibility to move among sectors, regions and market cap spectrums should be well-positioned to make the most efficient use of the listed infrastructure market. Listed infrastructure also provides investors with the flexibility to choose or amend their investment horizon and tailor liquidity preferences, sensitivity to short- term price volatility and choice of underlying asset risk exposure. It has performed consistently with unlisted infrastructure over the longer term, reflecting the stable and inflation-linked performance characteristics of the underlying assets and demonstrating its value as a complement to unlisted infrastructure.

1 All figures in U.S. dollars unless otherwise indicated.

2 Ofwat, as the UK water industry regulator, determines a real allowed return on assets (and an implied real post-tax return on equity). We have calculated an implied nominal return of equity allowed based on Ofwat’s implied real post-tax return on equity and the retail price index (RPI) as an escalator.

3 Given the lack of book equity, a function of the way the companies were privatised in 1990, a modified DuPont analysis has been undertaken to determine the reported ROE, as described in Exhibit note.