Join our daily newsletter At The Bell to receive exclusive market insights

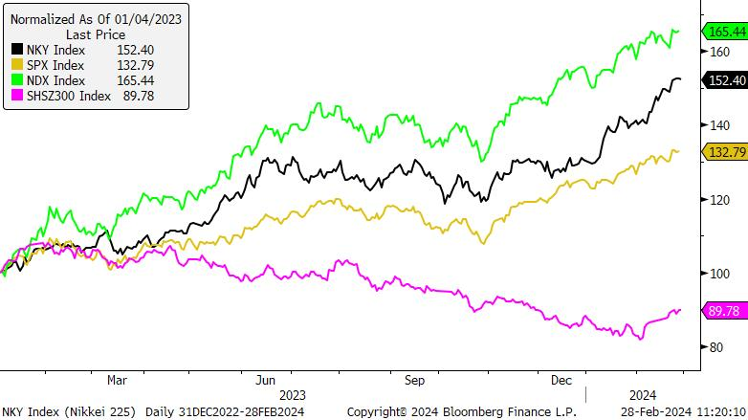

Japanese equities have been a focal point for global investors seeking growth opportunities and portfolio diversification this year, with the Nikkei 225 index recently breaching 35-year highs and climbing to fresh record highs above 40,000.

With the world’s third-largest economy boasting a rich tapestry of industries ranging from automotive and technology to healthcare and finance, Japan offers an array of investment options for discerning investors.

However, while the potential rewards of investing in Japanese stocks are enticing, navigating the intricacies of foreign exchange (FX) exposure remains a critical challenge.

Fluctuations in FX can significantly impact the returns of foreign investors holding Japanese stocks, adding an extra layer of complexity to their investment decisions, but appropriate hedging strategies can help investors optimise their portfolios for long-term success.

Why invest in Japanese equities?

Japan is a market where macro meets momentum.

Despite the challenges of an aging population, Japanese companies have for many years boasted large global operations and technological innovation, alongside a stable regulatory environment.

Some of the other tailwinds that have contributed to recent fresh highs in the Japanese equity markets include:

- A weak Japanese yen (JPY): A weak JPY can benefit Japanese exporters by making their goods more competitive in international markets, boosting export revenues and profitability. It also increases the value of foreign earnings when converted back into JPY, potentially leading to higher profits for multinational Japanese companies.

- Low interest rates: Japan is the only major economy that has negative interest rates. Despite expectations of normalisation for Bank of Japan (BoJ), we do not expect any significant increases to interest rates, which will continue to facilitate access to low-cost capital for the corporate sector. This environment incentivises borrowing for investment and expansion purposes, allowing Japanese companies to fund growth initiatives at favourable terms.

- Corporate governance reforms: Japan last year implemented significant corporate governance reforms aimed at enhancing transparency, accountability, and shareholder rights. These reforms included measures to strengthen board independence, increase disclosure requirements, and promote shareholder activism.

- The return of inflation: The exit from deflation in Japan has given pricing power to corporates, which is helping expand profit margins and increase capex spending. This could be the start of a positive feedback loop, as higher wages could drive up inflation further.

- Valuation discount: Japanese equities have long traded at a valuation discount compared to their global peers, presenting opportunities for value investors to acquire quality assets at attractive prices.

- Geopolitical risks: Japan has historically been a geopolitically stabilising force in Asia, contributing to regional peace and security. The country’s strategic alliances and diplomatic relationships have provided a peaceful alternative in the new normal of escalating geopolitical tensions. Geopolitical stability can attract foreign investment and foster confidence among domestic businesses.

- Tech innovation: Japan is at the forefront of technological innovation, particularly in sectors such as robotics, artificial intelligence (AI) and renewable energy. This offers the potential for significant long-term growth and profitability, especially in the current AI boom.

- Warren Buffett: The renowned investor and CEO of Berkshire Hathaway has expressed confidence in the long-term prospects of Japanese equities. His investments in Japanese trading companies, alongside his positive remarks about the country’s investment potential, have bolstered investor sentiment and drawn attention to Japanese market opportunities.

- Low interest rate sensitivity: The balance sheet of Japanese companies tends to be positive net cash (or negative net debt, or higher cash levels relative to debt), given the prolonged low interest rate environment. This means Japanese companies have a positive sensitivity to rising interest rates, unlike most other equity markets.

- Diversification: Investors exposed to the Japanese equity market are overweight to industrials and consumer discretionary sectors, and significantly underweight to the information technology sector. This has made the Japanese market a key consideration for those looking to diversify away from a large exposure to the “Magnificent 7” US tech stocks.

These tailwinds mean there are a number of opportunities in the Japanese market that investors can pursue. Some examples include:

- Large exporters and familiar names, such as Toyota, Sony, Nintendo, and Uniqlo’s parent company Fast Retailing.

- Semiconductor and chip stocks, such as Advantest, Tokyo Electron, Applied Materials, Screen Holdings, and Arm’s parent company Softbank.

- AI-connected software and data storage companies such as Fujitsu, NTT Data, CyberAgent, and Hitachi.

- Warren Buffet holdings, such as Mitsui, Itochu, Sumitomo, Mitsubishi, and Marubeni.

- Machinery and automation manufacturers such as SMC, Fanuc, Komatsu, and Mitsubishi Heavy Industries.

- Renewable energy companies such as Kansai Electric, Tokyo Electric Power, and Kyushu Electric.

- Exchange-Traded Funds (ETFs) such as iShares MSCI Japan ETF (EWJ), Global X MSCI SuperDividend Japan ETF (2564), and iShares Currency Hedged MSCI Japan ETF (HEWJ) offer a broad exposure.

Hedging your JPY exposure

FX risk is the potential volatility in the value of investments denominated in foreign currencies due to changes in exchange rates. In the context of Japanese equity investments, FX exposure is particularly relevant for foreign investors holding assets denominated in JPY.

The impact of FX exposure on Japanese equity investments is twofold.

First, currency movements can amplify or dampen investment returns, potentially magnifying gains or losses for foreign investors. A weakening JPY against the AUD means Australian investors receive fewer Aussie dollars when converting the returns of their Japanese equity holdings, potentially offsetting their positive returns.

If JPY weakness is significant, a foreign investor may still end up making a loss after converting their positive returns from Japanese stocks to their base currency.

Investors can look to forward contracts and currency options to hedge their exposure to JPY and safeguard their potential returns.

A long AUD/JPY position can both hedge FX exposure for Australian investors buying into Japanese equities, and also offer a positive carry return that can add to the overall returns. Currency-hedged exposures (such as via currency-hedged ETFs) can also help mitigate this risk, allowing investors to focus on the underlying fundamentals of Japanese stocks without being exposed to currency fluctuations.

Alternatively, investors can seek out the ‘natural hedge’ of investing in Japanese companies with significant global operations and non-JPY revenue.

Disclaimer:

Saxo Capital Markets (Australia) Limited (Saxo) provides this information as general information only, without taking into account the circumstances, needs or objectives of any of its clients. Clients should consider the appropriateness of any recommendation or forecast or other information for their individual situation.

The material provided in this article is for information only and should not be treated as investment advice. Viewers are encouraged to conduct their own research and consult with a certified financial advisor before making any investment decisions. For full disclaimer information, please click here.