Join our daily newsletter At The Bell to receive exclusive market insights

- Despite ongoing economic uncertainty, fintech disruptors are on the rise

- The combination of finance and technology has become a lucrative space in recent years, creating a pool of hungry, younger players

- Thus, in order to get ahead, disruptors must both compete and cooperate with their rivals: traditional banks and lenders

- They do this through warehouse lending, a system which provides emerging fintechs with funding and a critical endorsement

- So how have buy now, pay later giants like Afterpay (ASX:APT) and Zip Co (ASX:Z1P) used this system to their advantage, and which other fintechs are doing the same?

Despite ongoing economic uncertainty, fintech disruptors are on the rise. Lead by buy now, pay later stalwarts like Afterpay (ASX:APT) and Zip Co (ASX:Z1P), this fusion of finance and tech is out to challenge the big banks.

But to get ahead in an increasingly aggressive market, fintech stocks are turning to an unlikely ally: their competitors.

There’s a couple of ways a fintech can do this, but warehouse lending has recently emerged as an attractive option, thanks to the secure financing and endorsement it provides growing lenders.

So what’s in it for the companies which cooperate and compete with big banking? And which businesses have used this strategy to fuel their growth?

The fintech boom

In recent years, fintech stocks have garnered attention from investors and consumers alike. According to multinational accountant KPMG, global investors poured $25.6 billion into fintech businesses over the first half of 2020.

And while the fusion of finance and tech is a broad banner, it’s non-bank creditors which have recently come to the fore. Put simply, they can offer the ease of digital lending outside the parameters of traditional lenders — a key factor in their growing popularity.

As a result, the fintech revolution encouraged new players to join the space. But on the flip side, it also triggered market saturation, leaving some companies vulnerable to merger and acquisition activity. In its fintech trends report, KPMG predicted a spike in fintech consolidation over 2020’s second half.

“Fintech investors are focused on big bets and safer deals right now. This is making it difficult for smaller fintechs, even those with good business models, to raise funding.”

KPMG International’s Global Co-Leader of Fintech, Anton Ruddenklau

Faced with this ‘eat or be eaten’ proposition, just how do these companies get ahead?

Another option

While there’s a lot of competition in the digital lending space, companies are all peddling the same key message. A smaller fintech wants you to know it’s different from big banking — maybe it offers more personalised service, competitive deals, or better technology. In that way, a fintech can position itself in a ‘David and Goliath’ battle, poised to take on financial giants.

But the way this system works is somewhat paradoxical: to compete with the big banks, fintech disruptors need their backing. That’s because the banks have two things emerging lenders don’t: money and reputation.

Luckily for the fintechs, there’s a way to get both. And that’s where a warehouse facility comes in.

What’s that?

A fintech can approach a major lender and ask for a line of credit. If approved, a bank will set up a facility which the business can access. They’ll use that money to seed their own loan origination and grow their business.

As more customers borrow from the fintech, this business and the bank can profit off the lending.

In some cases, banks will use the fintech’s account receivables as collateral. So if the stock can’t pay back its borrowings, the bank can turn to its customers for the money instead. And as a digital creditor’s customer base grows, the bank can opt to expand or extend the funding facility.

Not only does the facility provide much-needed capital, but it also acts as a significant endorsement for an emerging business. The backing of a major bank can carry some serious clout. And in the case of BNPLs like Afterpay, the endorsement has paid off.

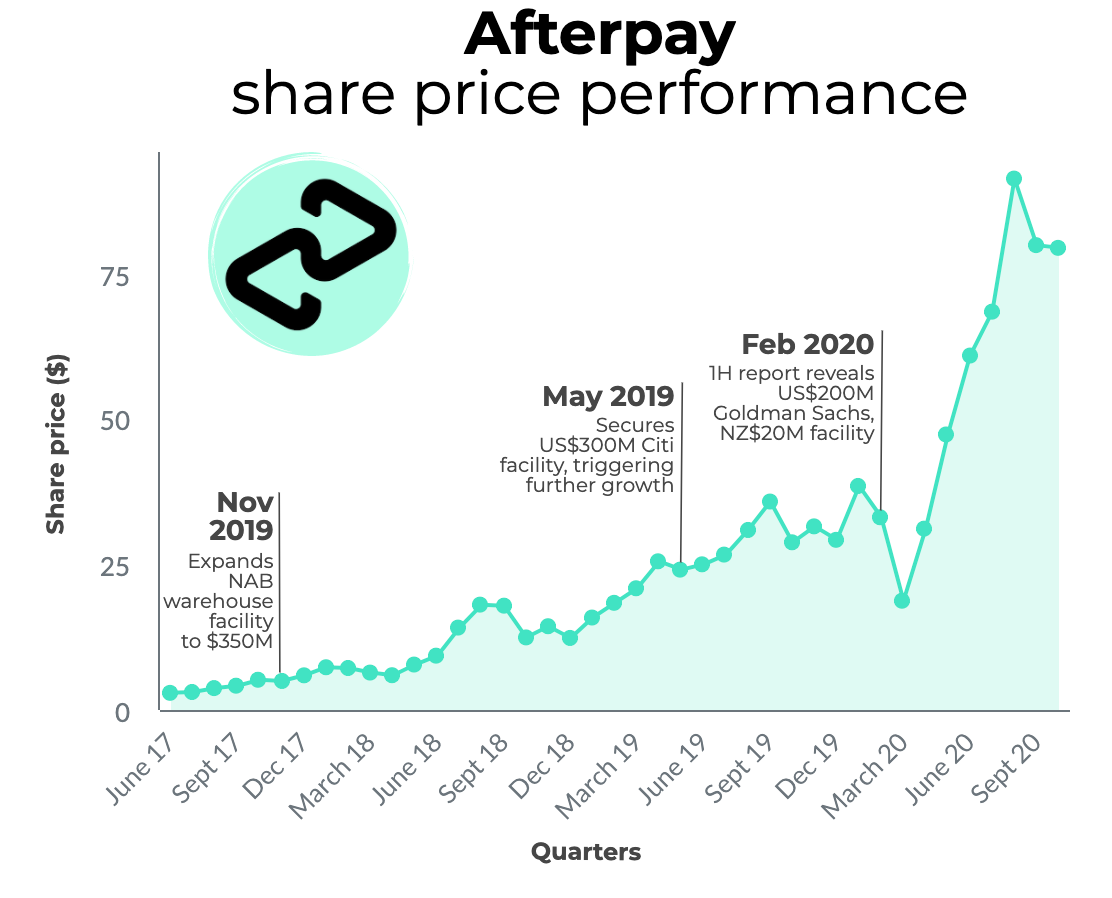

Afterpay

Afterpay — arguably the world’s buy now, pay later leader — had five warehouse facilities at the end of FY20.

Two of these are based in Australia, one is with a New Zealand lender, and the last two are with U.S. banks.

Combined, the two Australian facilities are worth half a billion, while both are set to mature in December 2022. Afterpay holds the covenants with National Australia Bank (ASX:NAB) and Citi, two leading lenders.

Over in New Zealand, Afterpay has a NZ$50 million (around A$46 million) warehouse facility with Bank of New Zealand. That’s set to expire in March 2022.

Afterpay’s other facilities, based in the states, total US$400 million (roughly A$562 million). These are with Goldman Sachs and Citi, and will expire in December next year and May 2022, respectively.

Curious to see how these facilities impacted the Afterpay share price? Here’s a graph which tracks the movement:

Interestingly, Afterpay’s NAB facility was set up before it listed on the ASX. And while the company hasn’t disclosed the start date for most of these facilities, it’s clear the financial endorsement set it up for its recent growth.

Conversely, the bank’s backing has also set this BNPL up to weather economic storms. When COVID-19 hit, Afterpay was quick to reassure holders its warehouse facilities were different from traditional debt covenants. And the continued backing of four brand-name banks — three of which are outside Australia — went a long way in steadying nerves.

After the initial market shock subsided in March, investors returned to the BNPL. And since April, it’s added roughly $50 dollars to its share price. Afterpay now boasts a $23.8 billion market cap and trades for $84.84 a share.

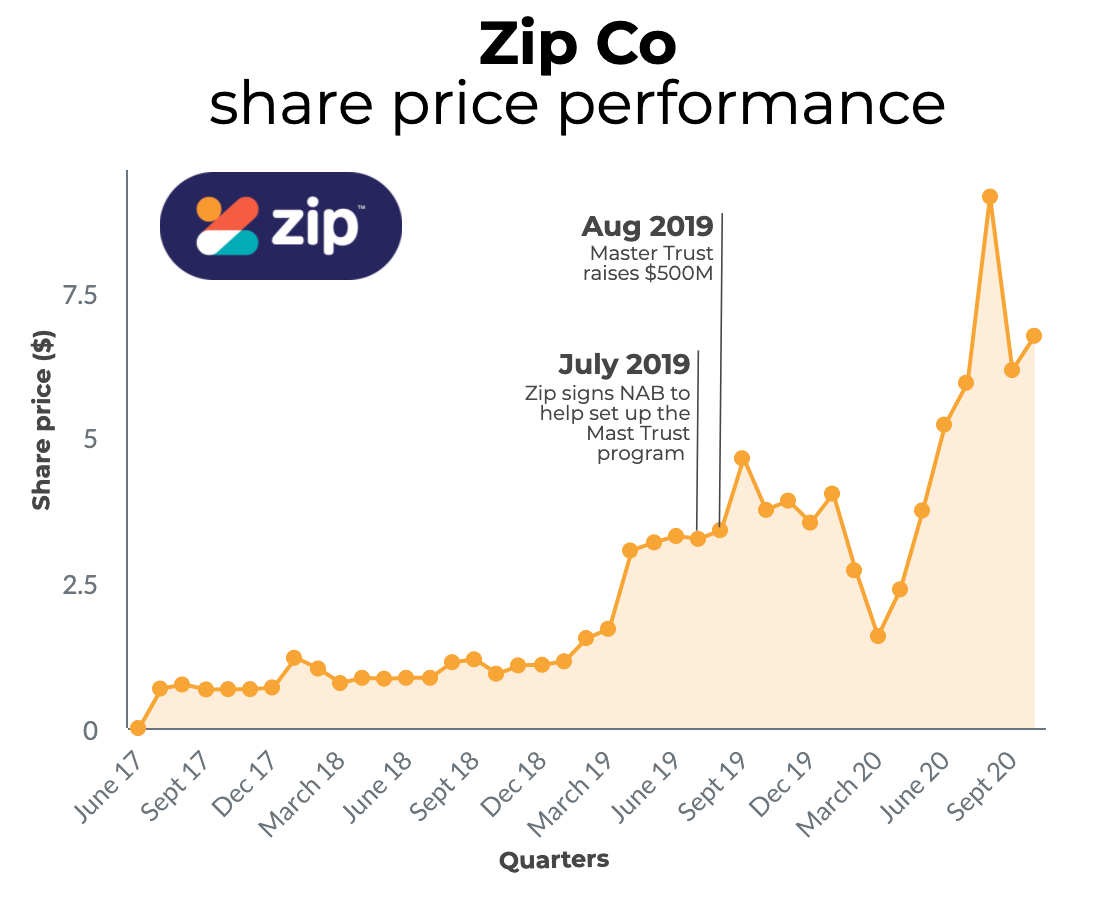

Zip Co

While Zip Co operates a little differently than Afterpay, it still has warehouse funding. In fact, during FY20, Zip secured a $100 million facility from Victory Park Capital, a U.S.-based investment firm.

But Zip has also proven it can work alongside the banks in a different way, and it’s made this its flagship funding structure moving forward. In 2019, Zip launched the Master Trust — the first of its kind for any BNPL in the world.

At the time, Zip — along with major bank NAB — raised half a billion by selling asset-backed securities to investors. The raise was an upgrade on Zip’s initial target — the fintech was originally looking to raise $400 million.

Here’s how that affected Zip’s share price:

After setting up the raise, Zip used the proceeds to buy a revolving portion of its account receivables debt — the money its customers owe — to keep in the Master Trust.

Essentially, money coming in from investors is paid back as the customer makes repayments. And as an added bonus, the risk on payment defaults is transferred from Zip to the noteholders.

This buoyed the BNPL stock as COVID-19 shook the local sharemarket earlier this year. And, like Afterpay, the funding facility positioned it for further growth as its customer base boomed.

Now, Zip has gone from a minnow to a unicorn. The fintech is worth over $3.76 billion today, with shares trading for $7.29 —a far cry from the $3.19 before the trust was set up.

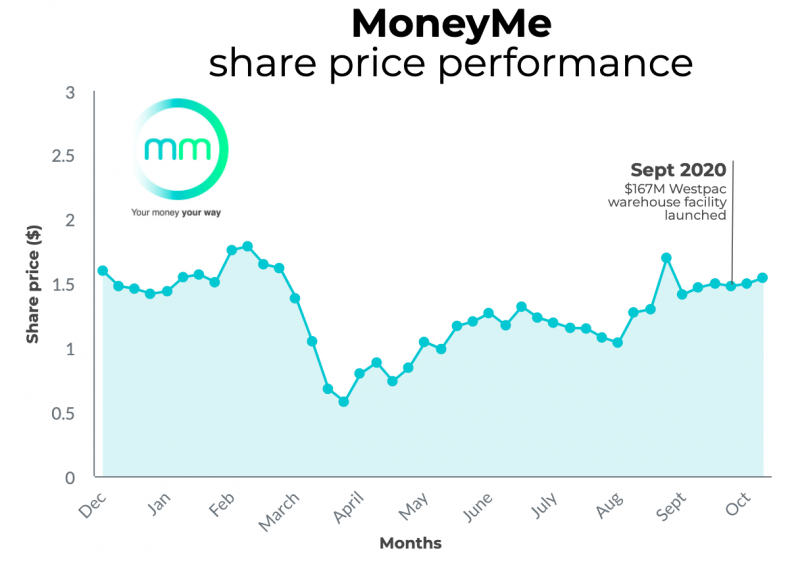

MoneyMe

While it may not be a BNPL stock, this fintech has also caught a big bank’s eye. Just last month, Westpac (ASX:WBC) created a $167 million warehouse facility for ASX lender MoneyMe (ASX:MME).

This is a big deal for the digital lender: it’s the first facility in its wheelhouse and paves the way for future growth.

“This major Australian bank partnership is transformative for MoneyMe, paving the way for substantial scale into the future,” Managing Director and CEO Clayton Howes said.

“This is a significant milestone that provides a step change in our funding costs, increases origination capacity and allows us to better compete on price,” he continued.

The deal is still fresh, so investors are yet to see the facility’s long term impact on MME’s share price. Here’s how the stock has traded to date:

Considering the financial turbulence triggered by the global pandemic, the deal’s significance is amplified. Moving forward, the backing of Australia’s oldest bank will go a long way.

Today, MoneyMe shares are worth $1.50. While it’s still trying to climb back to its mid-February high, one thing is clear: the deal has set the company up to grow its beyond 2020.

What’s to come?

As stocks across the globe continue to stage their recovery, funding and reputation become even more crucial. With the global pandemic decimating opportunity, it’s critical that businesses find new ways to keep afloat.

Smart fintechs will work with their competitors to overcome the hurdles and shine amid the turmoil. And the ones which grow will embrace the endorsement from traditional lenders and head on to bigger things.

Afterpay, Zip and MoneyMe have thrown down the gauntlet. The question remains: Who will be next?

-1200x645-380x200.jpg)